DEVELOPING AN EFFICIENT AND REPEATABLE LIFE CYCLE COST ESTIMATION PROCESS

Developing an Efficient and Repeatable Life Cycle Cost Estimation Process within an Integrated Product Team (IPT) FrameworkBY LOGAPPS LLC

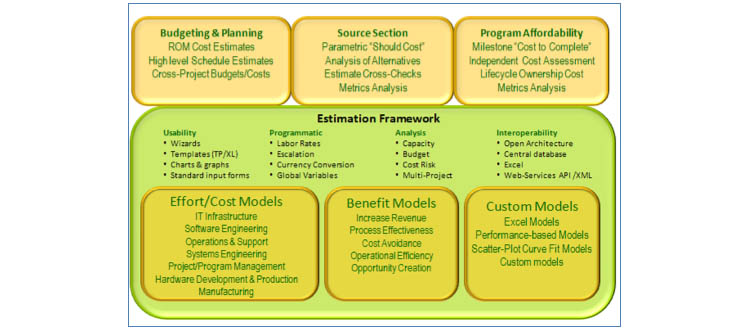

Logapps has developed an integrated Life Cycle Cost Estimation (LCCE) capability. for the Department of Homeland Security (DHS) Office of the Chief Information Officer (OCIO). We have leveraged parametric model (TruePlanning) and, cost estimation best practices.

We developed a three-tiered deliverable construct, including a Ground Rules and Assumptions Document (GRAD), Interim Estimate, and Basis of Estimate. The GRAD forces the PMO and sponsor to agree upon basic assumptions and methodologies, and when the estimate is briefed later, the team defends the process rather than the ‘number.’

TruePlanning, a parametric cost model, provided a framework for estimation that ensures all activities of the project were included, as well as embedded cost estimation relationships developed through the analysis of thousands of IT projects.

ensures all activities of the project were included, as well as embedded cost estimation

relationships developed through the analysis of thousands of IT projects.

SOFTWARE SIZING

Accurate software cost estimates are essential in the calculation of estimated project costs and schedules.

Software sizing is difficult for three main reasons: it is performed in a variety of contexts, software design documents vary in levels of detail, and software projects are often a combination of new, reused, and modified components.

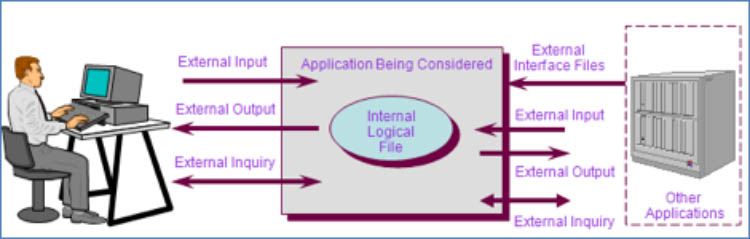

Function Points can generate size estimates from data available early in a project’s life cycle using detailed specifications. Function points are well-suited for size estimation from Use Cases, User’s Guide, or List of Requirements.

Our team followed a fast function point’ process, which followed International Function Point User’s Group (IFPUG) standards, and involved the following steps:

- Determine the Type of Count

- Identify Counting Scope and Application Boundary

- Count Data Functions

- Count Transactional Functions

- Determine Unadjusted Function Point Count

- Determine Value Adjustment Factor

- Calculate Adjusted Function Point Count

COST ESTIMATION BEST PRACTICES

While there is no one “right” process for ensuring quality cost and schedule estimates of projects, there are industry best practices. Two main sources used in our processes are:

- Carnegie Mellon University Software Engineering Institute (SEI) Checklists

- Government Accountability Office (GAO) Cost Assessment Guide

SEI Checklists: The SEI released two relevant special reports in 1995 on software cost estimation: A Manager’s Checklist for Validating Software Cost and Schedule Estimates [SEI-95-SR-004] and Checklists and Criteria for Evaluating the Cost and Schedule Estimating Capabilities of Software Organizations [SEI-95-SR-005].

The first document, [SEI-95-SR-004], provides seven key questions, and corresponding evidence characteristics, that should be explored when developing a software cost estimate. The seven questions are listed below.

- Are the objectives of the estimate clear and correct?

- Has the task been appropriately sized?

- Are the estimated cost and schedule consistent with demonstrated accomplishments on other projects?

- Have the factors that affect the estimate been identified and explained?

- Have steps been taken to ensure the integrity of the estimating process?

- Is the organization’s historical evidence capable of supporting a reliable estimate?

- Has the situation changed since the estimate was prepared?

The second document, [SEI-95-SR-005], provides two basic checklists: one for the requisites for a reliable estimating process; one for the indicators of an estimating capability. The requisites for a reliable estimate process are listed below.

- A corporate memory (historical database)

- Structured processes for estimating product size and reuse

- Mechanisms for extrapolating from demonstrated accomplishments on past projects

- Audit trails (Values for the cost model parameters used to produce each estimate are recorded and explained.)

- Integrity in dealing with dictated costs and schedules (Imposed answers are acceptable only when legitimate design-to-cost or plan-to-cost processes are followed.)

- Data collection and feedback processes that foster capturing and correctly interpreting data from work performed

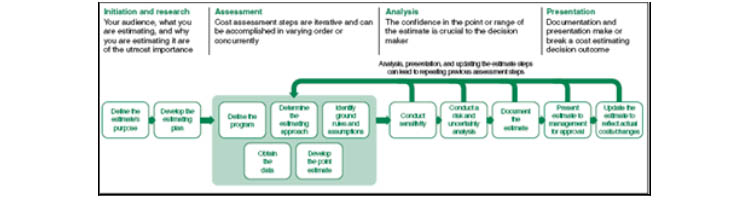

GAO Cost Assessment Guide: The purpose of the Cost Assessment Guide [GAO-07-1134SP] is to share generally accepted best practices for cost estimation. The Guide speaks specifically to the validation of a cost estimate by an outside organization, often in the form of an Independent Cost Estimate (ICE).

Figure 3 illustrates the estimation process presented in the Cost Assessment Guide, which maps well to our three-tiered deliverable process.

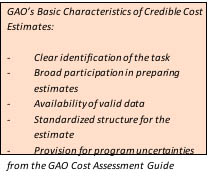

Four characteristics of high-quality cost estimates are identified:

- Well Documented

- Comprehensive

- Accurate

- Credible

The GAO Cost Assessment Guide also provides specific questions to be considered when reviewing software estimates. We use the followingf checklist in our internal QA process.

- Was the software estimate broken into unique categories-new development, reuse, commercial-off-the-shelf, modified, glue code, and integration?

- What input parameters-programmer skills, application experience, development language, environment and process-were used for commercial software cost models (such as SEER), and how were they justified?

- How was the software effort sized?

- How were productivity factors determined?

- What are the assumptions regarding code reuse, and are they justified?

- Were software maintenance costs adequately identified and are they reasonable?

CONCLUSION

Our team utilizes a parametric model and industry best practices to establish a repeatable, comprehensive, high-quality cost estimation process for each of our clients..

References

[CMMI 2007] CMMI: Guidelines for Process Integration and Product Improvement, Second Edition. Boston Massachusetts: Addison Wesley. 2007.

[GAO-07-1134SP] Cost Assessment Guide: Best Practices for Estimating and Managing Program Costs (Exposure Draft). US Government Accountability Office. GAO-07-1134SP. Washington, DC. 2007.

[SEI-95-SR-004] Park, Robert E., A Manager’s Checklist for Validating Software Cost and Schedule Estimates. Software Engineering Institute. Pittsburgh, PA. 1995.

[SEI-95-SR-005] Park, Robert E., Checklists and Criteria for Evaluating the Cost and Schedule Estimating Capabilities of Software Organizations. Software Engineering Institute. Pittsburgh, PA. 1995.

WANT TO LEARN MORE? CONTACT US TODAY